Ultimate Guide to Sinking Funds: Categories & Tips for a Happy Budget

One of the best ways to make your household budget more manageable is by using sinking funds. Sinking funds are categories that you add a little money to each month, so you don’t have to scramble to find huge chunks of money when a big bill comes.

This will make sure that you are never caught off guard by unexpected (or expected!) costs, and can continue living comfortably within your household budget.

Using sinking funds can help alleviate stress, prevent overspending, and keep your finances in order. In this blog post let’s talk about:

- What are sinking Funds?

- The essential sinking fund categories every budget should have,

- The magic formula to figure out how much to put into each sinking fund from your paycheck, and

- Tips for how to keep track of and use sinking funds effectively in your household budget.

What Are Sinking Funds?

Sinking funds are categories of money that you allocate to different expenses or savings goals. The idea is that a sinking fund grows a little bit at a time, so that when a big expense needs to be paid, you will have a nice, big chunk of money saved up to pay it.

You won’t need to panic trying to find the money all at once, or have to use credit cards or borrow, in order to pay the thing.

If you struggle with saving money, are just putting random amounts of money aside with no real goal, or have trouble figuring out how much money to put towards sinking funds, then keep reading!

Using Sinking Funds is a Healthy Addition to Your Household Budget

Sinking funds are a helpful addition to your household budget because they allow you to plan ahead, and save money for the future.

You don’t need a lot of extra cash to add sinking funds into your budget; just a small amount per month can make it much easier to handle big yearly bills, or reach future savings goals.

The most important reason to use sinking funds is because sinking funds provide STRUCTURE to your monthly budget. Bills that come once or twice a year like taxes, insurance premiums, etc. can be hard to pay all at once when you live paycheck-to-paycheck. Those bills can seriously derail your budget for months afterward.

But, if you are using sinking funds and setting aside a small amount from each paycheck for those bills, it will be much easier to pay them when they are due.

Sinking Funds Categories: The Essential Sinking Funds List for Any Household Budget

Really, any bill or savings goal can be turned into a sinking fund. There are many different Sinking Funds categories and as long as you have time between now and when the bill is due, you can start setting money aside for it.

However, I’ve found that these Sinking Fund Categories are the most essential to include in any household budget:

1. Emergency Fund

This sinking fund should be used in case of an emergency. The goal is to make sure that if something were to happen like a job loss or medical issue; your family would be able to pay your necessary expenses for at least three, and up to six months.

2. Holiday Shopping Expenses

This sinking fund is for holiday shopping that needs to be done. I love to add up what I spent the year before, and start putting money aside each month as early as January, so I don’t only rely on credit cards for gift-giving and food.

3. Vacation Fund

Saving up for a fun family vacation, an awesome road trip with friends, or a relaxing getaway with your partner not only makes it easier to afford, but it gives you all something exciting to look forward to.

4. Birthday Funds

Between gifts, balloons, entertainment, food and decorations, birthday parties can really add up. Having a stash of money on hand will make any event, big or small, run more smoothly.

5. Home Repairs

Appliances seem to break and leaks seem to spring at the absolute worst time. Stay ahead of them by keeping some money on the side. The best part of this particular sinking fund category is that if you don’t use it, you don’t have to keep adding to it.

6. Medical Co-Pays

Is it just me or are ALL medical bills super-high lately? I have to pay almost $2,000 to be seen in the ER, WITHOUT even being admitted. Having a small sinking fund for medical co-pays takes the financial strain out of the equation when deciding whether to get the care you need.

7. Child Care

For example summer camp, nursery school, or a babysitter for times when the kids are on vacation (but you aren’t).

8. Self Care

Like hair salon, massages, hair removal, etc.

9. Car Repairs/Replacement

Depending on your car’s specific warranty, you may need to pay for wheel alignments, cracks in your windshield, tire repair or replacement, etc.

10. Life Insurance Premiums

These bills come up yearly, and can sometimes be anywhere from $500 to over $1,000. If you have children or a spouse/partner who does not work, a term life insurance policy is very important to have.

11. Local/State/Federal Taxes

If you are self-employed or work on commission, you may have to pay quarterly estimated taxes. Setting aside a little money out of each paycheck will take the sting out of having to make that larger tax payment each quarter.

Other Sinking Funds Examples

Like I said before, really any bill or savings goal can be turned into a sinking fund, you only have to set aside a little bit of money at a time.

Here are some other examples to add you your sinking funds list if it makes sense to:

- Children extra curricular activities

- Pet medical expenses

- Back to school expenses

- Annual gym memberships, if not paid monthly

- College Tuition for your children, IF you are already contributing to your own retirement

Calculate How Much You Should Put in a Sinking Fund With This Easy Sinking Funds Formula:

How much should you put in a sinking fund? The answer is right here in this formula.

It’s the easiest way to figure out exactly how much money should be going into each sinking fund category from your paycheck.

This sinking funds calculator will tell you how much you need to save each month to make sure you have what you need when that expensive purchase comes.

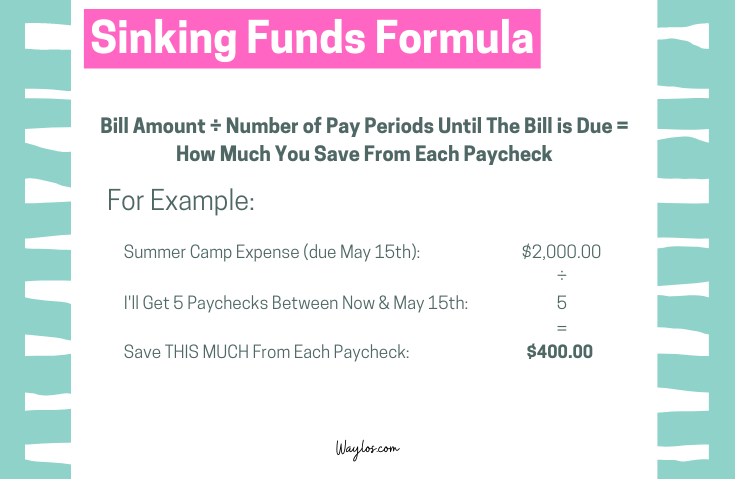

The short story for sinking funds is this: you take the amount you are saving for (for example you are saving $2,000 for summer camp & the bill is due May 15th) and divide it by the number of times you get paid between now and when your bill is due.

Let’s say you get paid every two weeks, or “bi-weekly.”

Using the summer camp example, between now and May 15th, let’s say you have five pay periods (in other words, you get paid five times between today and the bill’s due date).

You divide $2000 (the bill amount) by 5 (the number of times you get paid between now and May 15th), and get $400. That’s how much you take out of every paycheck & keep in your account (or transfer into your savings, or put cash in an envelope), so by May 15th you’ll have the $2000 to pay the bill when it’s due.

So,

bill amount ÷ number of pay periods until the bill is due = how much you take from each paycheck.

Now, in a perfect world, you have extra money after paying your bills & variable expenses, and you’ll have that $400 in every paycheck to save. That isn’t always the case, like a lot of times one of your paychecks is going to rent or mortgage and that’s a big expense, and you have less leftover to save.

There may be times you will have to divide up that $400. So maybe it’ll have to be that you save $200 one pay period and $600 the second pay period, to get to $2,000 by May 15th. It all depends on how much money you have leftover from your paycheck after your fixed bills are paid.

For Savings Goals That Don’t Have a Due Date:

The best way to start a sinking fund for expenses that don’t have a due date, but you want to be prepared for, and calculate how much you want to put in each pay period, is to estimate what you may need. Some questions to think about include:

- Are any of my appliances under warranty, or out of warranty?

- What year was my home built, and what is the useful life of the big parts of it (windows, roof, pipes, boiler, water tank, sprinkler system, etc?) A google search would help give a rough idea of how long before your home needs to be updated.

- Is my furniture under warranty? Do I have pets or small children who may bounce on or stain anything?

- Is my car still under warranty or not?

How To Pay Monthly Bills with Sinking Funds

Utilities and other monthly bills: This is a very interesting sinking fund category. It’s perfect for families who don’t have a regular paycheck, and maybe get paid in large chunks, for example commission payments.

In this case, instead of putting small payments into your sinking fund each pay period, you can take a larger percentage of money to be able to pay for a few months of a particular bill.

Doing this takes the pressure off of not knowing when your next payment will come in. It’s like having a cushion for your expenses.

For example, you can put big chunks of money into a sinking fund for your utilities at the beginning of each year. Just know what you spent the previous year, and add 5 or 10%. Then, you can use a specific bank account to put that money in, and have your bills on auto-pay.

Where to Keep Your Sinking Funds

There are several place you can keep your sinking funds money:

- your regular bank account (which will be mixed with your regular spending)

- One separate bank account to keep all of the money (I suggest a high interest savings account)

- A separate bank account for each sinking fund category (so several bank accounts)

- A cash envelope or for each category, if you prefer to use cash instead of the bank

Retirement and education funds should really be invested and earning interest. If your employer doesn’t have a retirement program you can contribute to, then asking a financial adviser is the best way to go here.

How Should You Organize Your Sinking Funds?

Keeping track of the money in your sinking funds categories may sound hard, but it’s actually really easy!

Here are some tips and tricks for staying organized:

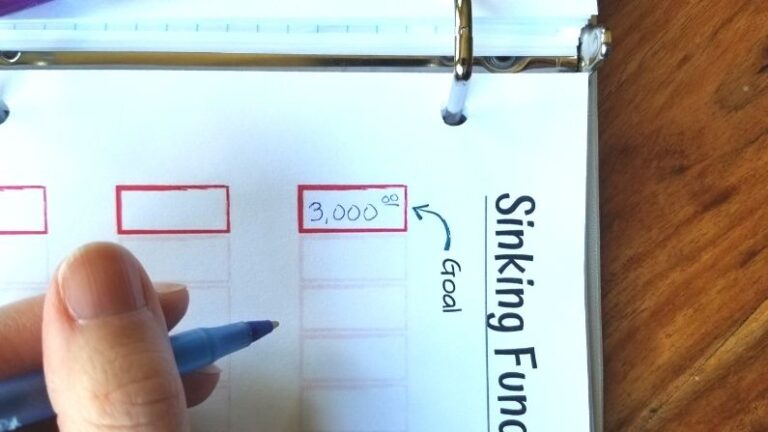

1. Use a Spending Fund Tracker to Record Your Deposits

If you are working with cash, some cash envelopes or cash envelope inserts would be perfect for keeping a running tally of your deposits.

If you are keeping your money in the bank, a sinking funds tracker would be perfect:

Plus, with a sinking funds tracker you have the added bonus of watching your funds grow, it’s very motivating and helps keep the momentum going to continue to save.

2. Use a Free App for Bank Accounts

Another option for when you keep money in one or more bank accounts, is downloading a free app like Mint or Personal Capital, or a paid app like You Need A Budget. You can categorize each deposit, or split a deposit into several categories. The app will take care of adding up the total, or subtracting once you use some of the money to pay your bills.

3. Make Sure You’re Tracking Your Sinking Funds at Each Pay Period

This way, each sinking fund category can be tallied up at the end of the year.

This will make it easier to see how much money is in each category, and whether you are hitting your savings or expense goal. as well as if there should be more or less put into any specific fund.

Whatever system you use, make sure it’s easy to see how much money you’ve set aside for each fund. The simpler it is, the more likely you are to stick with your system.

Make Your Budget More Predictable & Smooth With Sinking Funds

A sinking fund is a budget category that provides for periodic expenses or savings goals. Sinking funds are a top priority in any monthly spending plan so that you can be sure you have the money necessary for your big expenses or savings goals at the time they are due.

If you’re still struggling with how best to use this strategy in your personal finances, take a look at my Premium Budget Binder Printables on Etsy, which includes my Sinking Funds Tracker.

I hope these sinking funds ideas help make managing your budget and saving for those big expenses easier and more achievable going forward!

XO,

-Mina

PS: Here Are Some More Blog Posts You May Find Helpful: